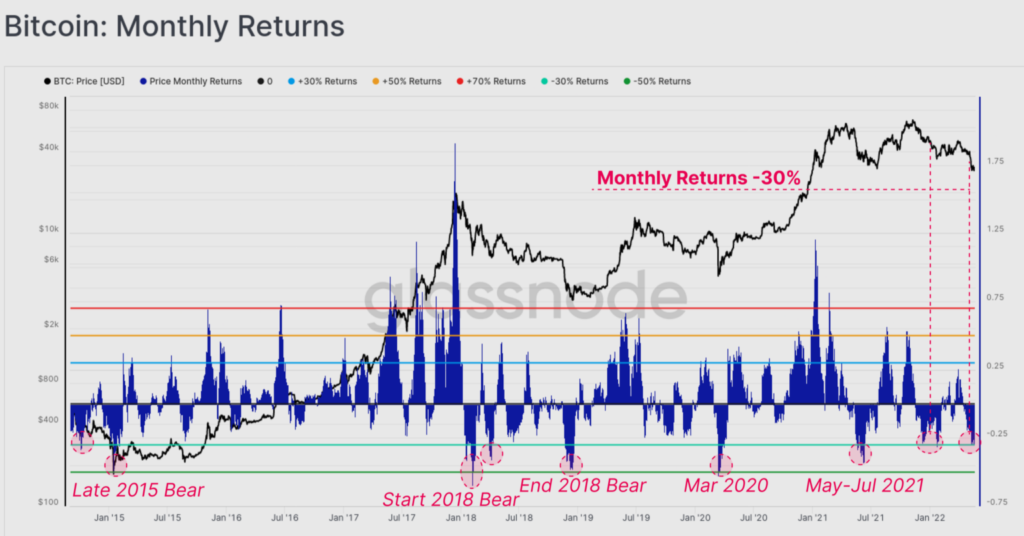

The Bitcoin market has now traded lower for eight consecutive weeks, the longest continuous string of red weekly candles in history. Even, Ethereum, the largest altcoin painted the same picture. Well, such bearish movements directly or indirectly affect the returns/profit margins.

To make matters worse, derivatives markets suggested fears of further decline at least for the next three to six months.

Diminishing returns

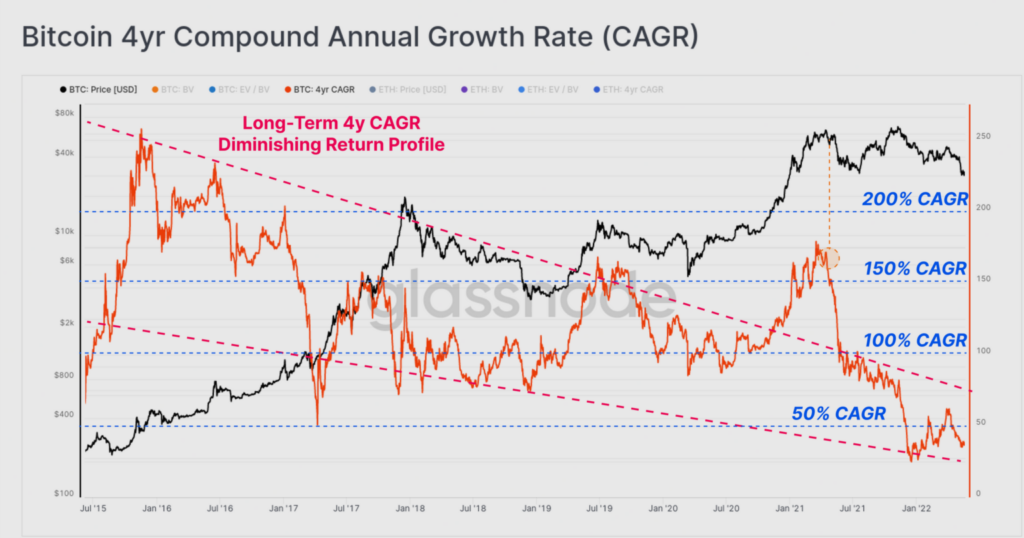

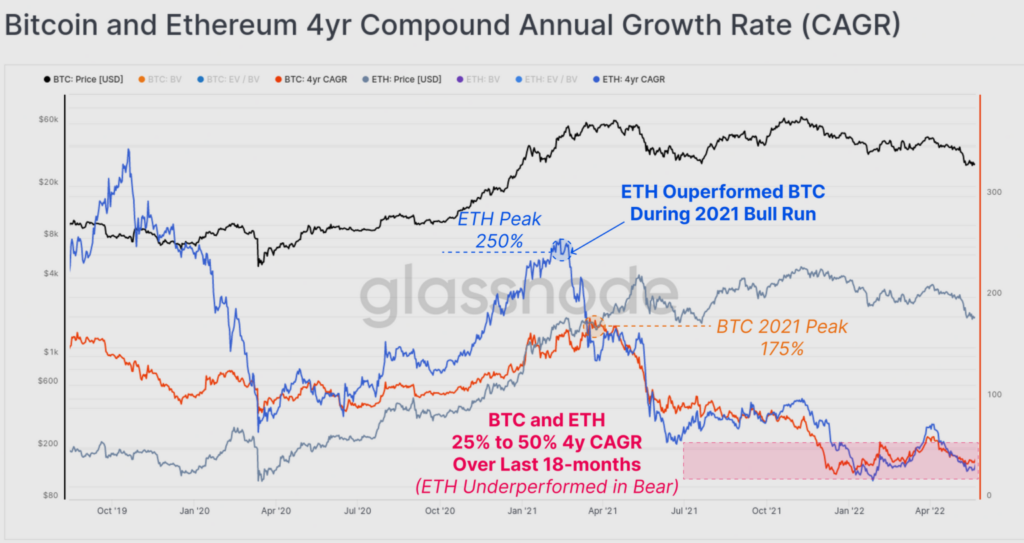

Price-performance over the last 12 months has been nothing short of lacklustre for both Bitcoin and Ethereum. Indeed, this put a dent in long-term CAGR rates for Bitcoin and Ethereum. Glassnode’s weekly report published on 23 May highlighted this scenario.

Considering the largest cryptocurrency, BTC has been trading in a roughly 4-year bull/bear cycle that is often associated with halving events. When it comes to long-term yield compression, the CAGR has fallen from 200%+ in 2015 to less than 50% at the time of this writing.

The report added,

“In particular, we can see the marked decline in 4y-CAGR following the May 2021 sell-off, which we have argued was likely the genesis point of the prevailing bear market trend.”

Additionally, Bitcoin gave a negative 30% short-term return, meaning it corrected by 1% on average on a daily basis. This negative return is quite similar to previous bear market cycles for Bitcoin.

Moving on to ETH, the altcoin recorded relatively poorer performance compared to BTC. The monthly return profile showed Ethereum recorded a grieving picture of -34.9%. In the longer run, Ethereum also seems to be experiencing diminishing returns over time.

Additionally, over the past 12 months, the 4-year CAGR for both assets has dropped from 100%/yr to just 36%/yr for BTC. Also, 28%/yr for ETH, underscoring the seriousness of this bear.

The report further added,

“ETH has generally outperformed BTC during bullish trends, however these divergences do appear to be getting weaker over time (lower upwards divergences). In more bearish trends, it can be seen that the ETH CAGR often tends to underperform BTC.”

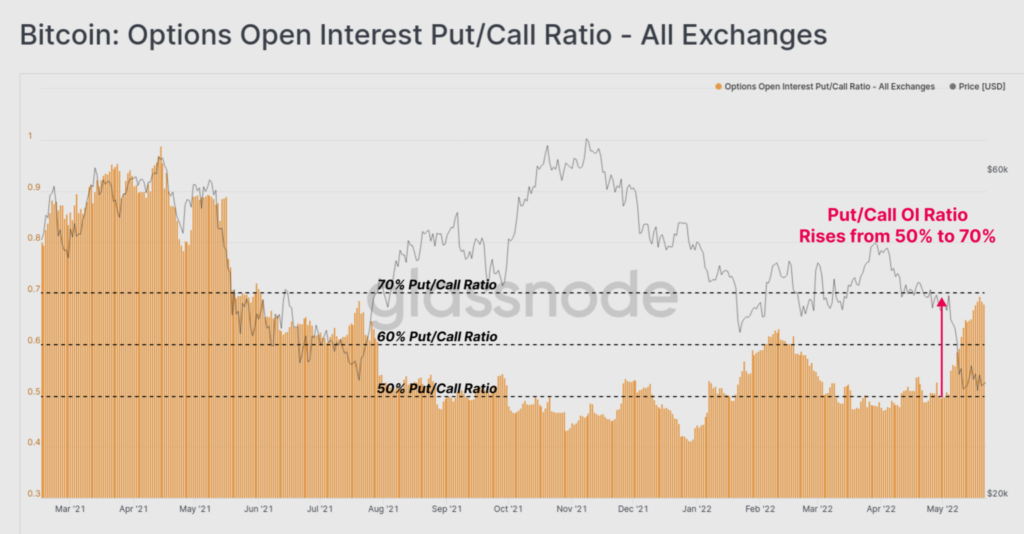

To make matters worse, the derivatives market warned of a further market decline. Options markets continue to price in near-term uncertainty and downside risk, especially over the next three to six months. In fact, implied volatility saw a significant increase last week as the market sold off.

Notably, with such a heavy bear market in play and unimpressive price performance, it is no surprise that the market had a notable preference for Put options. The Put/Call Ratio for open interest increased from 50% to 70% over the last two weeks, as the market seeks to hedge further downside risk.